Heading one

Heading two

Step One: Build Your Knowledge

Why is Financial Information Important to Your Business?

If you're going to be in business, you must know how to keep track of what you earn and what you spend. Bookkeeping software has made tracking your financial activities easier than ever. With some basic knowledge and support from a professional tax accountant, you can take care of most of the day-to-day bookkeeping yourself. Once you understand basic accounting, it also makes it easier to work with a professional bookkeeper if you decide to hire one.

You may have heard the statistic that, according to the Small Business Administration (SBA), roughly one in five businesses will fail in their first year. Only about half of all new businesses will make it to five years, and only 30% of businesses will make it to year 10. The two biggest reasons for business failure are lack of sales (the market doesn’t know about or doesn’t want the products or services offered) and cash flow—not having the cash needed to meet financial obligations when it is needed. Fortunately, both those problems have simple solutions. And, it is absolutely worth the effort to solve those challenges because the SBA also tells us that on average, self-employed people are generally significantly wealthier than regular employee workers.

So, how do you keep yourself from becoming a statistic? Easy. Know your numbers and have a cash management plan.

Small business financial needs are very different from those of large corporations, but the terminology is all the same, so let’s start with some definitions.

What is the Difference Between Bookkeeping and Accounting?

Accounting refers to the bigger picture, where your financial transactions and financial information are combined in standard reports, or financial statements. These standard reports help you (as well as partners, lenders, advisors, and other stakeholders) understand the financial health of your business so you can make wise financial decisions. Bookkeeping is the basis of accounting. A professional accountant, also referred to in this session as a tax accountant, will gather the information from the bookkeeper (either the hired bookkeeper or the business owner) to create financial statements, prepare tax reports, and file taxes on behalf of the business.

What are Financial Statements and Why do you Need Them?

Financial statements are the standard reports every business prepares to summarize financial information to give a complete picture of the business.

The three most important financial statements are the Balance Sheet, the Profit and Loss Statement, and the Statement of Cash Flow.

The Profit and Loss Statement, also called the Income Statement, shows how your business earned and spent money, and if the business is profitable or not.

The Balance Sheet shows how much the business is worth, including everything others owe to the business (assets), everything the business owes to others (liabilities), and everything the business owns (equity).

The Cash Flow Statement summarizes the movement of cash and cash equivalents (like credit card and loan payments) that come in and go out of the company. The Cash Flow Statement measures how well a company manages its cash (money) and if the company generates enough cash (money) to pay its operating expenses and debts.

As a business owner, you need to feel comfortable understanding what each of these reports is telling you about your business. These reports will help you make better financial decisions and keep you from getting into a difficult financial situation.

EXAMPLE: Landscape Services LLC

Landscape Services LLC is a company that provides landscaping design and construction to homeowners. It is a small company with one owner and two employees and annual revenues of about $190,000. The Profit and Loss Statement for Landscape Services LLC (PDF) shows revenue from design services, landscaping services, and the sale of materials and plants to customers. Expenses include the cost of materials and plants, salaries and wages, and other operating expenses like utilities and fuel. Income before taxes and interest was $13,349 and after taxes and interest was $10,754.

Profit and Loss Statement Example

Landscaping Services, LLC

| Landscaping Services, LLC | |

|---|---|

| Profit and Loss, July 1, 2024 to June 30, 2025 | |

| Revenue | |

| Design services | $18,666.00 |

| Landscaping services | $133,855.00 |

| Materials & plants sold | $37,800.00 |

| Total Revenue | $190,321.00 |

| Expenses | |

| Cost of materials & plants sold | $22,000.00 |

| Owner salary | $52,000.00 |

| Employee wages | $68,000.00 |

| Advertising | $1,250.00 |

| Fuel | $2,587.00 |

| Insurance | $1,200.00 |

| Legal & accounting fees | $1,500.00 |

| Office rent | $24,000.00 |

| Utilities (gas and electric) | $900.00 |

| Phone | $1,200.00 |

| Software subscriptions | $900.00 |

| Miscellaneous | $1,435.00 |

| Total expenses | $176,972.00 |

| Net income before taxes and interest | $13,349.00 |

| Taxes paid | $2,250.00 |

| Interest paid | $345.00 |

| Net income after taxes and interest | $10,754.00 |

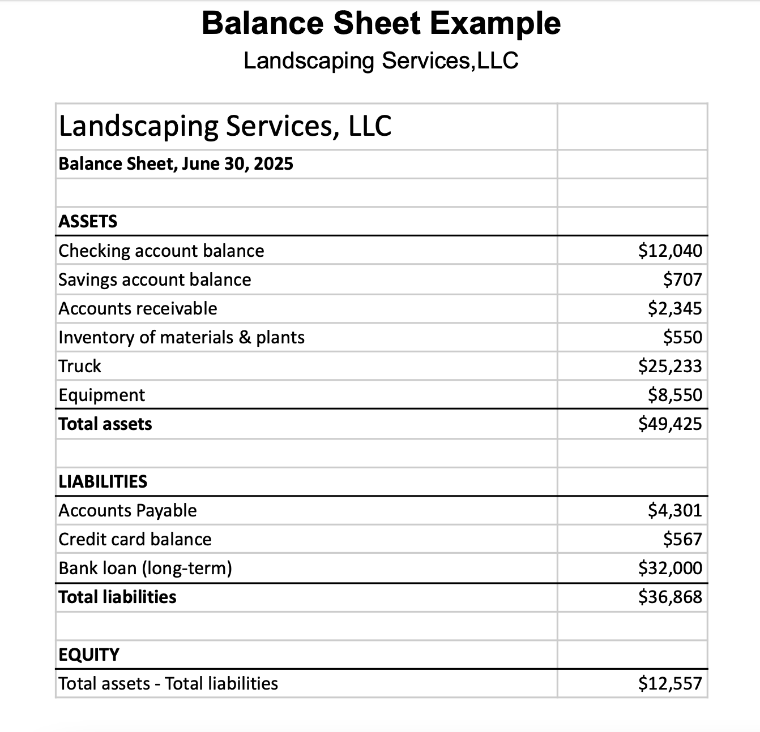

The Example Balance Sheet for Landscape Services LLC (PDF) shows the assets and liabilities of the company on a specific date, June 30, 2025. The main assets are cash in the checking and savings accounts, accounts receivable (money owed to the company), inventory of materials and plants that have not been used yet, a truck, and equipment. The company’s liabilities are accounts payable (money owed by the company to suppliers – probably unpaid invoices), a credit card balance (money owed to the credit card company), and a long-term loan (perhaps for the truck).

The difference between the assets and the liabilities is the equity in the company - basically how much the company is worth, on this day, based on this short list of assets.

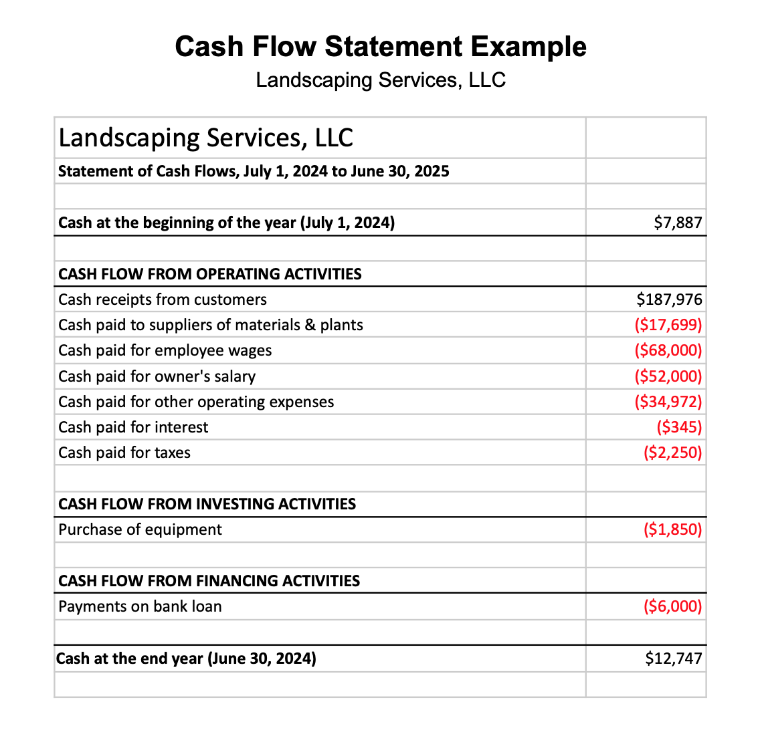

The Cash Flow Statement for Landscape Services LLC (PDF) shows how cash was collected and spent over the course of the year. It starts with the cash on hand (in the checking and savings account) at the beginning of the year, July 1, 1024. Cash coming in and going out for operations, investments, and financing are added or subtracted from the starting cash to calculate the ending cash balance, on June 30, 2025.

Cash flow from operating activities is cash going in and out for operations – all the activities associated with providing goods and services to the company’s customers during the year. Cash receipts for the year were $187,976. To generate these sales, the company incurred expenses for materials and plants, wages and salaries, other operating expenses, interest, and taxes. All are shown on the cash flow statement.

In addition to the cash used for operating activities, cash was used for investing (purchasing equipment) and for financing (payments on the outstanding bank loan). The cash flow statement shows that there was $12,747 at the end of the year after adding and subtracting the movement of cash in and out of the company.

While this cash flow statement covers an entire year, it is common for small businesses to create monthly cash flow statements to monitor the flow of cash in and out of the company more frequently.

How do I Keep Track of all the Financial Information I Need?

The best way to keep track of what you earn, what you spend, what you owe, and what you own, is to set up a bookkeeping system to organize your receipts and transactions. As a general rule, it’s a good idea to keep all receipts and bank statements for three years.

If you are a solopreneur or a sole proprietor, operating your business on your own, you may choose to create a process where you place every receipt or bill in a designated spot in your home or working space, and once a week you enter the expenses and payments on a piece of paper or spreadsheet. It is important to keep careful track of all the dates, amounts, reasons for the expenses, and to save all your receipts. It can be helpful to make notes directly on receipts or invoices as you get them to keep track of the business purpose of the expense or payment .

You may also decide that it’s helpful to bring your bookkeeping online with some bookkeeping software like Quickbooks, Xero, Wave, or others. An advantage of bookkeeping software is that it can track everything in one place by connecting your transactions with your business bank account. Most software even allows you to upload photos (taken with your smartphone) or files (PDFs) of your receipts, so you don’t have to keep track of the paper receipts any more.

No matter what system you use, you will need to start with a customized Chart of Accounts to define the accounting categories you will use when entering your transactions.

The Chart of Accounts

The Chart of Accounts is a list of all of the accounting categories you will use to record how you earned, spent, moved, and kept your money. Usually your chart of accounts will have an account for every line on your balance sheet and every line on your profit and loss statement. Most bookkeeping software comes with a default Chart of Accounts that suggests the different types of accounts you will need.

Not every business has every type of account. The best way to start a chart of accounts is to think of where you earn money, how you spend money, and where you keep your money and then make sure you have accounts to match. For example, if you send invoices to customers, then you need an account for Accounts Receivable. If you borrowed money for your business, then you need an account for long term liabilities. It is a great idea to get a professional bookkeeper to review your Chart of Accounts with you!

Let’s start by defining accounts from the profit and loss statement. Then we will take a look and define some accounts that are appropriate for more complex businesses.

Profit and Loss Statement Accounts

Every business has sales and expenses, so every business must have accounts to keep track of sales revenue (or income) and other accounts to keep track of business expenses.

- Revenue and income accounts

- Service Revenue or Income accounts: In service revenue or income accounts you keep track of money earned by the business through sales of services. While you only need one income category to track your sales, it can be helpful to specify your different revenue streams so you can see how your different activities bring in money. For instance, if you are a musician, you may wish to track your revenue from teaching music separately from your revenue from playing music. If so, you would want two different service revenue accounts.

- Product sales revenue or income: In product sales revenue or income accounts you keep track of money earned by your business from selling goods or products. As with service revenue you might want to separate revenue accounts for different goods. For example, if you are a grocer, you might have different revenue accounts for the sales of fresh vegetables and the sales of baked goods.

- Other Income: If your business has bank accounts, it will probably earn some interest. If you sell an asset for more than you bought it for, then you have a profit. “Other income” is a place to keep track of this kind of revenue, sometimes called “unearned income.”

- Operating expenses and expense accounts: Of course, you will have expenses associated with producing the goods and services that you sell. Operating expenses are expenses associated with operating the business. Typical operating expenses include:

- Salaries expense: Expenses associated with employees who receive a salary. Usually the owner’s salary is included in this account.

- Wages expense: Expenses associated with employees who are not salaried and receive an hourly rate of pay.

- Supplies expense: Expenses associated with supplies used during the month or year.

- Rent expense: Expenses associated with using a rented building or office.

- Utilities expense: Expenses associated with electricity, heat, water, and sewer used during the month or year.

- Telephone expense: Expenses associated with your telephone.

- Advertising expense: Expenses for advertisements, promotions, coupons, and other promotional items.

- Depreciation expense: Costs of long-term assets allocated to expense during the current month or year (typically you will need the assistance of an accountant to determine depreciation expense).

- Cost of Goods Sold (COGS): The Cost of Goods Sold is a special category of accounts that reflect those expenses that are directly related to making and delivering products to customers. Sometimes it is helpful to have accounts for each of the expenses that makes up the COGS, and sometimes it is better to aggregate it all into one account. The two main components of COGS are the cost of materials in producing a good and the cost of labor in producing and delivering a good. In general, a business needs to keep track of Cost of Goods Sold only if it carries inventory. You should consult with your accountant on the necessity for COGS accounts.

The accounts described above are common for many small businesses. The list does not include all possible accounts and you should consult with your bookkeeper and accountant to make sure you are keeping track of all your revenues and expenses.

Balance Sheet Accounts

A complete chart of accounts typically includes items from your balance sheet. The three categories of accounts on your balance sheet are assets, liabilities, and equity.

Assets include all your bank accounts where you keep cash, accounts receivable, current assets (things that you intend to sell or use during the year, like inventory), and fixed assets (things that last more than a year and depreciate, like vehicles, equipment, and furniture). Liabilities include accounts payable, credit card balances, current liabilities (things that you need to pay during the year, like quarterly taxes), and long-term liabilities (like long term loans). Equity accounts include net income (the amount of profit or loss for the year), retained earnings (the amount of all prior year profit or loss that is retained by the business), and owner’s equity (the amount of cash taken from the business by the owner or loaned to the business by the owner).

The importance of these balance sheet accounts depend on the size and type of business that you have. For more complex businesses, it will be important to get the assistance of an accountant to select which accounts are needed by your business and how to calculate the balances.

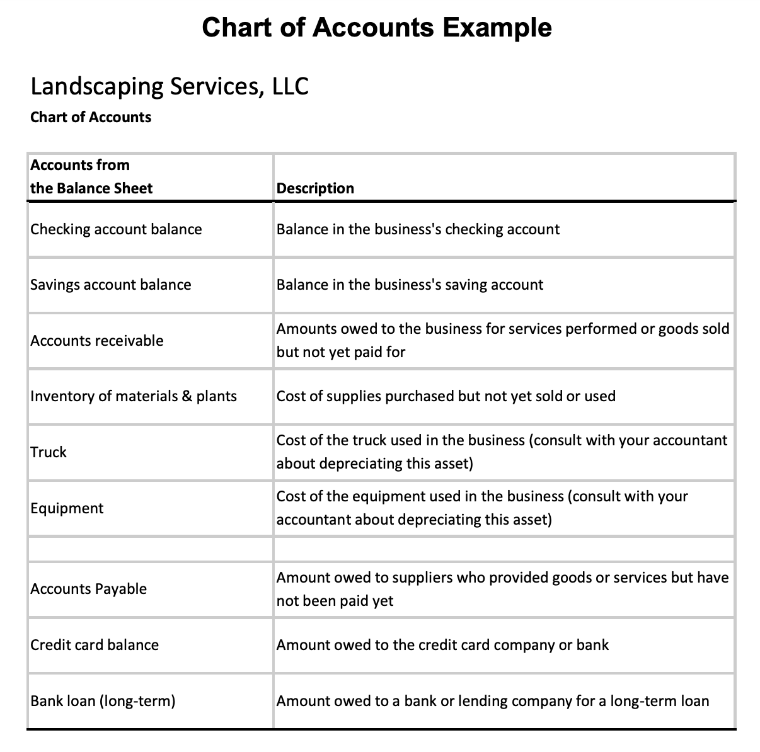

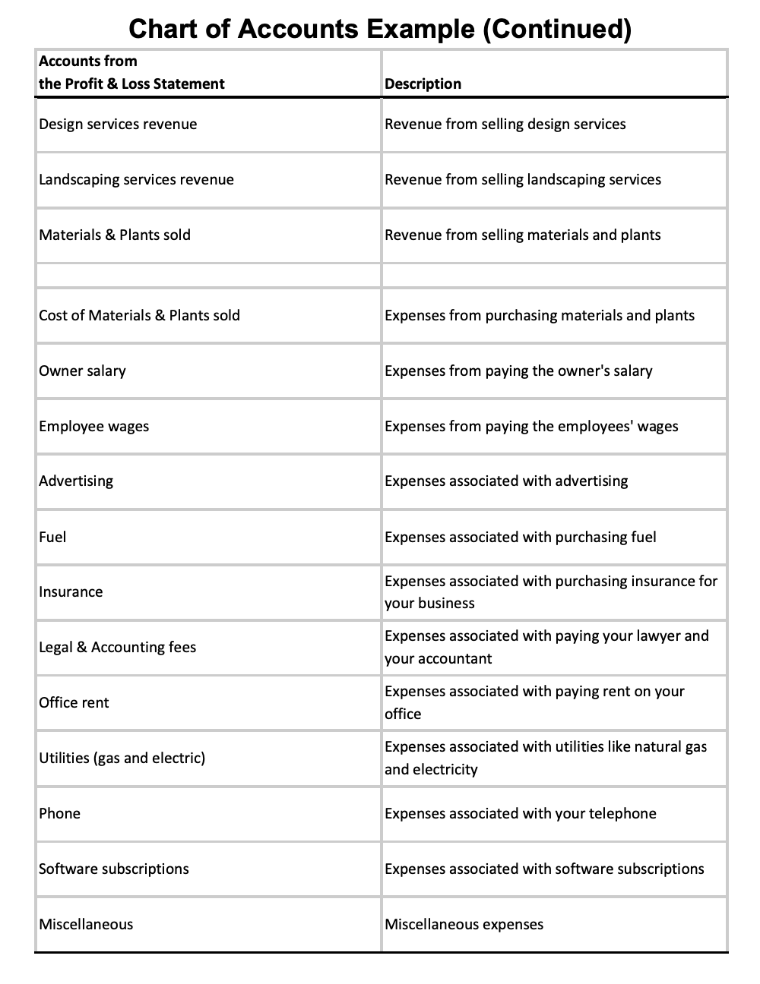

You can see the Chart of Accounts for Landscape Services LLC (PDF) here.

How to Track What is Important

It can be overwhelming to look at a Chart of Accounts and know how much detail is enough and how much is too much detail. Here are three guidelines to help you determine if something deserves its own accounting category:

- Do I care?

- Is it big enough to matter?

- Can I do anything about it?

Do I Care?

If you can’t think of any reason you care about what your different marketing expenses might be, for example, then there is no reason to get into too much detail. For example, you might not care about whether you were spending money on printing promotional materials online advertising, or another marketing activity. Double-check with your tax accountant to make sure they don’t care too!

Is it Big Enough to Matter?

Sticking with the marketing example, let’s say you would like to see how much you are spending on print advertising versus pay-per-click advertising online. But, when you look more closely at your spending habits, you only print out promotional flyers once a year and spend less than $100 on printing. So it isn’t really big enough to make a difference if you stopped spending on flyers. I define “big enough to matter” as the answer to the question “If I had to cut expenses dramatically, would cutting this make a difference to my profit?”

Can I do Anything About it?

There are some expenses that we can reduce by negotiating, shopping around for suppliers, or being frugal. And, there are others, like utilities, that we don’t have a lot of influence over. So, even if you were paying a lot for water and electricity, you probably can’t choose where you get your water and power. So it wouldn’t make sense to give these expenses separate accounting categories in the Chart of Accounts. I’d suggest keeping it simple and just calling them both Utilities.

Methods of Accounting

There are two main methods of tracking income and expenses - Cash Accounting and Accrual Accounting. These are two different ways of tracking and looking at how you earn and spend money in your business.

Cash Basis Accounting Method

Cash Accounting is the simpler of the two methods, reporting income when the cash (money) is received and expenses when they are paid.

When you look at your reports on a Cash Basis, you get a good understanding of how cash is actually deposited and distributed.

Accrual Basis Accounting Method

Accrual Basis Accounting is based on entering or reporting income when it is earned, even if it has not been collected (for example if you provide a service for which you send an invoice to be paid within 30 days, you would enter the amount you are owed on the day you provided the service). Similarly, expenses are entered or recorded when they are incurred, even if they have not yet been paid.

When you look at your reports on an Accrual Basis, you are looking at your earning potential (what you sold) and spending obligations, which can give you a better idea of what an average month should look like.

In the US, a business only files taxes on an Accrual Basis if they carry inventory or have more than $25 million in sales for three years.

Most bookkeeping software allows you to look at reports on both Cash and Accrual, but if you don’t use invoices or bills, your reports might look exactly the same.

For example, if you make a sale to a customer on terms, meaning they don’t have to pay you for a certain amount of time, you would enter an invoice to track the sale (income) and the Account Receivable. When the client pays, you would record a payment to show the Receivable had been paid. Between the time that the invoice is recorded and the customer pays you, your income is called Accrued Income.

Let’s say the invoice was recorded on September 30th and the client made payment on October 15th. If you looked at your Profit and Loss report on a Cash Basis, you would see the income in October, when the invoice was paid. If you ran the Profit and Loss on an Accrual Basis, the income would show in September, when the sale was made.

The same is true with expenses. If a vendor provided you with service and sent you a bill and you recorded that amount due as an Account Payable in August but actually paid the bill in September, Accrual Basis would show the expense in August. On a Cash Basis your income statement would show the money spent in September.

There may be some special considerations in managing your money through the transition between one tax year to the next and how best to account for income earned and expenses incurred in one calendar year but not paid until the next year. A tax accountant can help provide guidance in this area.

Keeping Business and Personal Money Separate

It is very important to keep your personal and business money separate. One of the first things you should do when starting a new business is to create a separate business bank account. It is ok to have a credit card in your name that you only use for business purposes, but you want to avoid using one credit card for both business and personal expenses.

It is important to remember that in many countries your business is a separate legal entity. One of the steps in establishing your business is to create and register a fictitious business name, or your “doing business as” (DBA) name (see the Licenses and Permits session in this course for more information). Even if your business name just adds the word “photography” or “construction” to your name, it allows you to create separate finances and accounts for your personal life and business. Your clients will then make payments to your business name, and an established name will help your business look more professional.

If you were to get investigated (audited) by an agency like the Internal Revenue Service (IRS) in the US, you are likely to have both your business and your personal finances examined. Any questionable deductions would probably be denied if you don’t have good separation and record keeping. Good accounting records are key to your financial success.

For expenses that are partially business use of personal resources, like auto mileage and home office, it’s important to understand how these deductions can be claimed. You should always pay these expenses in full from your personal account and reimburse yourself the deduction from your business, or have your tax accountant claim the deduction when you file your tax return.