Computer screen displaying a financial graph showing financial gains and losses. Photo by Pexels at Pixabay.

Edward Sorensen ’25 graduated from SCU with a double-major in finance and philosophy, and a minor in mathematics. He was a 2024-25 Hackworth Fellow with the Markkula Center for Applied Ethics. Views are his own.

Introduction

Every decision we make, whether consciously or unconsciously, is informed by our ethical values, including those in business.

While ethics has always been emphasized in the finance classes I’ve taken, it’s also always felt like a filter; a secondary condition to check after formulating a course of action to ensure it meets minimum legal requirements or standards of socially acceptable behavior. Ethics is more than a tool for compliance, it’s a fundamental component in making good business decisions.

This article seeks to elucidate that connection. By considering conclusions from behavioral psychology regarding human behavior and decision making, and linking them to empirical evidence from interviews with professionals from across the finance industry, I will make the case for why ethics complements finance.

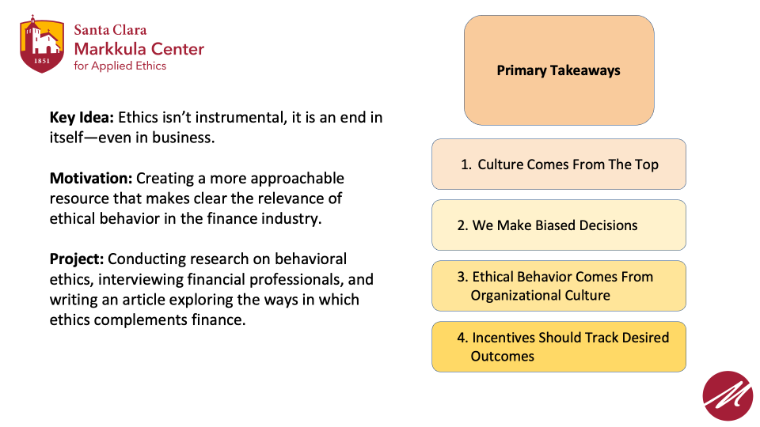

The key idea here is that ethics isn’t instrumental, that it’s an end in itself. Good ethical behavior across an organization generally leads to the development of better companies, not only in terms of social responsibility, but in sustainable long-term profitability.

Motivation and Methodology

My general motivation going into this project was to better clarify the ethics-finance connection and determine where exactly finance professionals and behavioral psychologists see ethics manifesting in finance. I interviewed four finance professionals—a professor of behavioral finance at SCU; an assistant treasurer at a fintech company; a director at a venture debt firm; and a managing director at a large asset management firm—representing the academic, corporate, venture capital, and banking sectors while tying in the psychological elements informing decision-making across the field. I supplemented this with research into bias and heuristics, alongside theories of business organization, to better contextualize my empirical findings.

Abstract

Four primary takeaways flow from my interviews and research: that culture comes from the top, that we make biased decisions, that ethical behavior comes from organizational culture, and that incentives should motivate desired outcomes. These four takeaways combine to describe how ethics works at an organizational level, and provide insight into how to optimally structure ethical financial ecosystems.

Findings

Culture Comes From the Top

The idea that culture comes “from the top” was shared by everyone I spoke to. Phrases like, “the tone really gets set at the top,” and, “tone at the top is actually very important,” were emphasized by interviewees from both academic and professional backgrounds. But what drives this belief? One effect is practical—the C-Suite makes the rules that apply across firms and hires the individuals enforcing them. They also play a formative role in firm mission statements and strategic plans, the ideals and goals held in each directly influencing employee behavior.

Besides legally having leadership duties and decision-making authority, the actual way that leaders behave also bears weight. Oftentimes, this is informed by their own ethical convictions, and can lead to good and bad outcomes.

One good outcome is exemplified by the airline company Southwest, who for several decades was the most profitable airline company while following an ethic of care model as their primary business plan.

Per the Markkula Center for Applied Ethics Framework for Ethical Decision Making, care ethics holds “that options for resolution must account for the relationships, concerns, and feelings of all stakeholders.” In doing so, care ethics centers interpersonal relationships and makes use of empathy to appreciate “the interest, feelings, and viewpoints of each stakeholder,” using “care, kindness, compassion, generosity, and a concern for others to resolve ethical conflicts.”

In Southwest’s case, the airline’s ethic of care model centered both employees and customers, treating them like family members rather than means to the end of shareholder profitability. Per one of my interviewees, in the company’s early years, their CEO intended to “find a way to build a culture [such] that the feeling of the company is of people wanting to be good to each other.” They built a culture “that tried to be respectful of their customers, meaning passengers [and] give them a good experience.” This entailed giving passengers “what they were expecting, which was a comfortable flight and bags not lost [...] [while helping] them feel good during the flight.” This approach was also applied to their employees, with flight attendants being trained to cover for each other while in service and remain “highly personable, humorous, [and] caring” while in service.

By orienting their corporate culture around caring, Southwest fostered a sense of belonging and community, creating a network of loyal customers and employees, who respectively committed to returning in the future or found purpose in their work, driving decades-long success.

A bad outcome is exemplified by the tech firm HealthSouth. The CEO’s relentless focus on meeting Wall Street expectations ultimately led to falsified financial reporting and the company’s collapse. This approach is marked by a more egoist conception of ethical behavior, where one’s own financial wellbeing trumps the social role the business is expected to play and the transparency of public information intended to improve market efficiency and minimize the risk of investors being lied to and taken advantage of. Former HealthSouth CFO Aaron Beam commented in a 2018 interview, The Slippery Slope to Corporate Corruption, that HealthSouth’s CEO “very much wanted to become a billionaire” and “created a cult-type environment” centered around accommodating his desires. Beam noted that “you say yes because if you said no, if you said no, it's a bad idea; he literally would beat you up.” In doing so, he undid any checks and balances provided by other corporate officers or the company’s Board of Directors by bullying them into submission. He prioritized personal wealth and power, driving him to disregard his obligations as CEO to other stakeholders—whether that be shareholders, investors, other employees, or the public at large.

Another bad outcome brought up by the venture debt director I spoke with is that of Elizabeth Holmes and Theranos. The person I spoke with pointed out that Holmes, to an extent, saw herself to be “this successful Steve Jobs-esque Stanford dropout” to the point that “[she started] to not realize where the lie [was] anymore” en route to “defrauding investors and wire fraud.” In this case, Holmes’ ethical incentives may not have been outright malicious—at least per his reading of her case—but the tone at the top created an environment in which an unethical outcome, albeit one motivated perhaps by delusion rather than greed, was generated.

With these examples in mind, the key takeaway here is that organizational culture essentially flows from the standards, policies, practices, and role modeling of those who lead organizations.

We Make Biased Decisions

While many of us are aware of bias conceptually, we may not be aware of the extent to which it informs our decisions. The fact is, we, humans, are all biased. This is simply by virtue of how our brains work. Whether we’re consciously aware or not, we’re subject to a wide variety of cognitive biases that lead us to make the decisions we make. I’ll outline several key examples from behavioral finance professor Hersh Shefrin’s book Behavioral Risk Management below.

The SP/A theory (security, potential, and aspiration), posits that emotion plays an integral role in how people make decisions. First hypothesized by psychologist Lola Lopes, SP/A theory is based on experimental results indicating that when people make risky decisions, emotions like fear, hope and the feeling of ambition play a key role in the actual decision they make. Lopes suggests that individuals make choices among risky alternatives based on the competing psychological needs to “assuage fear by providing security,” “offer hope by providing upside potential,” and be successful, “by achieving a predefined aspiration level or goal” (Shefrin, 25).

In the context of finance, SP/A theory suggests that the environment in which employees make decisions directly informs the decisions they make. For example, employees will be more risk-averse when fear is a more dominant emotion, and more risk-seeking when hope is a more dominant emotion. It’s worth noting that these emotions exist on a spectrum, and that not every individual will respond to these stressors in the same arbitrary way. Even so, the central claim, that our emotions inform our rational decision-making processes, holds true regardless of instantiation.

Another notable bias is the endowment effect, which describes how people tend to attach higher values to objects they already possess versus objects they don’t already possess (Sheffrin, 31). This is similar to status quo bias, which describes the common preference for maintaining an established behavior or condition rather than changing it. Both of these factors inform our stubbornness to give up previously held beliefs and belongings. In finance, this could manifest in commitment to an older way of modeling or doing business, or to an attachment to an enshrined culture or set of values—even if that culture or set of values is outdated, offensive, or just generally suboptimal.

Prospect theory, developed by psychologists Daniel Kahneman and Amos Tversky, asserts that people “interpret events through the lens of gains and losses relative to some ‘reference point’”, suggesting that people tend to overweigh small probabilities versus large ones, and no risk versus little risk (Shefrin, 37-38).

The ethical implication of this is that these reference points skew the way individuals make decisions. An asset manager, for example, might skew the allocation of a client’s portfolio on account of their perception of the risk it bears. This could potentially conflict with their fiduciary duty to best represent their clients’ interests should their read on risk be out of line with the actual risk of the portfolio.

It’s also worth noting that the overweight of small probabilities could also incentivize ethical behavior—for example, dissuading individuals from embezzlement on the grounds that they could be caught and punished. Like nearly all biases, prospect theory is ethically neutral in itself, but by virtue of the impact it has on decision making, it’s necessary to consider its potential influence when making decisions.

Framing is the phenomenon in which the decisions we make tend to be directly shaped by the manner in which information is presented to us. Shefrin cites an example where an individual accepts an even bet for $225 dollars under one framing and rejects it under another (Shefrin, 44-45). In the first case, the bet is offered directly following a loss of $750 dollars. In the example, the bet is accepted under this framing. In the second case, however, the individual chooses between a loss of $750 dollars, or an even chance at losing either $525 or $975. The bet is rejected under this framing. In both cases, the probabilities and dollar amounts stay the same—the wording of the choices changes, and as a result the outcome is generated. Coupling the experimental evidence that people respond to situations differently depending on their unique psychological characteristics and emotions at the time, with the revelation that simply the manner in which information is conveyed can change the way an individual responds to a question.

The above examples are just a survey of the many biases currently being researched by behavioral psychologists that inform human decision making. All of them, however, play key roles in how we make decisions in the workplace. This fact is ethically neutral, neither good nor bad for those ignorant to it, but doesn’t justify ethically wrong behavior. We should be self-aware of the way we’re programmed and recognize that our internal values—especially those related to ethics—are grounded in these well-defined, not necessarily logical modes of thought. Having this self-awareness helps us better understand why we reach the conclusions we reach, and allow for more thorough self-reflection on our decision-making methods and their relationship with ethics going into the future.

Ethical Behavior Comes From Organizational Culture

The previous two sections have dealt with the overarching structures informing behavior and decision making within organizations. In this section, I will place more focus on what drives individual ethical behavior within organizations. Namely, that is organizational culture. While organizational culture comes from the top, it’s that organizational culture that informs individual ethical behavior on a day-to-day basis. This is a function of framing bias. Essentially, the ethical standard set across the company is generally the standard employees will index their decision-making around, regardless of other external ethical influences.

One of my interviewees spoke about the Wall Street Journal (WSJ) test, which was employed and taken seriously across the large investment bank at which he started his career. The WSJ test entails reconciling that any one individual can do “far more to damage [a] firm than [they] can ever do to help it.” It’s centered around the idea of considering what would happen if “your actions and activities and decisions showed up in a headline on the Wall Street Journal.” The main idea here is that the firm’s culture was centered around this notion of accountability, and the idea that when you make a decision, you should broaden your perspective beyond the immediate consequences, to what would happen if the world were to watch it. In this case, individual ethical behavior is incentivized by forcing individuals to reconcile their decision making with the broader implications of social judgment.

This indexing doesn’t necessarily need to be around a test. A cultural emphasis of more vague concepts like teamwork also informs individual behavior. One interviewee shared an experience they had at a Big-4 accounting firm relating to this sentiment. She noted, “you’re working in teams, and you're out at the client site” the “whole general sentiment is [that] nobody goes home until the full team is ready to go home for the day.” In this case, individuals index their behavior around cohesion as a team, which, while less explicitly ethical, affirms at least a minimum sense of responsibility shared between team members.

This orienting of individual behavior to organizational culture can also generate more cutthroat environments where broadly ethical outcomes aren’t incentivized. One of the interviewees discussed a hypothetical scenario in which a firm is built around internal competition. He paralleled it to the expertise-sharing culture at his workplace, where “there’s no reason I shouldn’t try to help [a struggling coworker],” conceding that in other organizations, “some people wouldn’t do that [...] especially if there’s infighting in a firm [...] it’s like let's see this guy try to figure it out.” In this case, organizational culture would be built around individual success. Community would be disincentivized and workers would sink or swim, make ethically just, or ethically unjust, decisions completely on their own behalf.

More holistically, one of my interviewees noted that, “what is it that really induces people to want to behave ethically in [a] company, [... is it that it’s] what [they are] expected to do. [The] informal cultural issues [...] go hand in hand with what’s written on paper.” To them, culture seems to be the direct source of ethical behavior in their workplace.

Ultimately, with these lived experiences in mind, organizational culture seems to directly influence the kinds of actions individuals decide to take within organizations.

Incentives Should Track Desired Outcomes

Generally, nearly every financial scandal, from Enron to HealthSouth to the subprime mortgage market failures before the 2008 Financial Crisis, can be traced back to misaligned incentives. In the first two cases listed above, the issue was triggered by firms prioritizing stock price or Wall Street projections over legality, transparency, and sustainable long-run competitive strategy. The same prioritization occurred before the 2008 Financial Crisis, just with the priority being the quantity of mortgages sold.

Incentive misalignment prevents businesses from fulfilling their core requirements to stakeholders. But what exactly are these incentives in the first place, in what sense are they ethical, and how do we make them track desired outcomes?

Before discussing incentives, it’s first relevant to consider a few more ethical lenses pertinent to individual action in corporations. Three especially relevant lenses, per the Markkula Center Framework for Ethical Decision Making, are the common good, justice, and virtue lenses.

The common good lens refers to the notion that community life is “a good in itself.” This approach views respect and compassion for other members of society as essential, and pays special attention to the “common conditions that are important to the welfare of everyone”. Basically, the common good lens prioritizes actions that mutually benefit all members of the community. In the finance world, this might look like corporate transparency—creating a marketplace where investors and competitors are confident that they can trust the information available as they make decisions.

The justice lens refers to the idea “that people should be treated as equals according to some defensible standard such as merit or need.” This doesn’t mean that everyone should be treated identically, but rather that individuals deserve what they’re “due” for the actions they take. In finance, this might look like fair and equitable compensation, grounded in merit and appropriately distributing the value generated by different employees and their decisions.

Lastly, the virtue lens asserts that “ethical actions ought to be consistent with certain ideal virtues that provide for the full development of our humanity.” Virtues, per this lens, “are dispositions and habits that enable us to act according to the highest potential of our character and on behalf of values like truth and beauty.” The virtue lens suggests that by cultivating and practicing virtues in everyday action, we not only behave ethically but feel happier and live more meaningful lives. In the realm of finance, especially pertinent virtues might include courage, integrity, and self-control, especially with regard to decisiveness and rational decision making.

These three lenses frame our discourse around incentive misalignment. While they can be interpreted in different ways, generally, we would consider incentives misaligned if they drive individual action that is not ultimately in the interest of the common good, is unjust, or doesn’t cultivate the virtues associated with the good life. The Classical Greek philosophers who developed this view called this good life eudaimonia—the non-instrumental feeling of long-term happiness and fulfillment accompanying the living of a virtuous life.

With this in mind, what specific incentives are at play in the financial industry?

One interviewee identified three primary incentives: monetary compensation, promotion, and personal and professional development, an “umbrella term [for] growth or learning.” She felt that “if the incentive for an individual is truly the learning and the growth [...] I don’t see that one being at odds with ethics very much, I think it’s more so when you’re trying to compete for something that is scarce and limited, that’s where the opportunity for ethics to be compromised would even come up, not that it necessarily does, but that’s where it could, versus if you are just solely trying to learn and grow.”

The ethical implications of the above three incentives vary. Monetary compensation and promotion are necessarily scarce in almost every business environment, and confer social benefits. As a result, all the aforementioned lenses become especially relevant: because of this associated social benefit, the temptation to prioritize compensation and promotion opportunities over work could drive improper employee decisions—at least with regard to the common good and merit- and need-based considerations.

This scarcity, however, doesn’t seem to apply to development, which is necessarily indexed on an individual level. Development, then, seems more appropriately linked with the virtue lens, and the associated idea of cultivating one's virtues as an end in themselves, not as a means of attaining some other worldly goal.

Another one of my interviewees viewed incentives in a more transactional manner, as the general reason why someone should go out of their way to take an action. “When I hear incentive, I usually think tit-for-tat, or more like what are you going to give me to do something, kind of thing.” This view aligns incentives with the justice lens; it characterizes incentives as proportionate responses to previous decisions, offers, and policies. Like the previous characterization of compensation and promotion, tit-for-tat incentive structures are also open to misalignment. Should individuals prioritize more egoistic selfishness, or disregard their obligations to other stakeholders beyond the involved parties, this could drive outcomes that aren’t just—like overly excessive executive compensation—or are not in the common good—for example, rating subprime mortgage-backed securities (MBS) highly, locking in kickbacks along the sell-side of the mortgage market, but giving investors false impressions of their reliability.

Another interviewee also saw incentives as compensation, but saw that as manifesting in two real manners: “there's economic compensation and there's psychological compensation.” Economic compensation refers to the monetary compensation listed above, with its role being instrumental—as a means of attaining other life goals. Psychological compensation, however, more closely mirrored the “development” incentive previously discussed. This was especially pertinent in his discussion of finance generating a “significant amount of psychological satisfaction” through being a “fascinating game.” The interviewee commented that he feels that competitive people are drawn to finance, and that part of the reward comes from “[finding] the best investments” and “[doing] the very best analysis and diligence to decide as to whether there’s a return.” This psychological satisfaction could be framed as the practicing of virtues generating eudaimonia. By finding ideal investments and making decisions, finance professionals can practice the courage, integrity, and self-control virtues I highlighted earlier, among others, in the process of actualizing one’s competitive spirit and being one’s true self. This interviewee also makes it clear that the incentives he sees to be applicable in finance might not be universal across all industries, just that, from his experience, in the finance industry, “that just happens to be how [incentives work] for us.”

My last interviewee discussed incentives in the context of principal agent theory—a way of thinking about structuring incentives to incentivize the right thing. The three aforementioned interviewees all thought about incentives in marginally different ways. Even so, there were overarching similarities—on one end, more instrumental goals oriented towards money and power, and on the other, psychological satisfaction and internal personal development.

Per my last interviewee: the central question facing firms in the finance industry is: “how do you build companies and compensation systems [...] that serve the money well, that give you an incentive to use the money well, to serve the interests of the real people who are putting up the money [...] and have them behave in ways that make them good stewards of other people's money?”

The goal here is incentivizing behavior ethically aligned with a firm’s mission and competitive goals and in line with the needs of all relevant stakeholders. Viewing corporate policy and culture through the lens of satisfying the aforementioned incentives of power, money, and personal and psychological development provides one pathway to doing this. By applying the ethical frameworks discussed above, considering framing bias, and processing the primary motivators of individuals in finance, systems designers can leverage incentives to drive ethical behavior, rather than creating systemic misalignment that generates crisis.

Conclusion

Ethical behavior is incredibly relevant in the finance industry. From leadership at the executive level, to biases on the individual level, organizational culture, and corporate incentive structures, ethics plays an integral role in the way any given business operates. Given its economic significance, and lucrative access to both social status and wealth, it’s important to promote ethical behavior across the industry to ensure just outcomes. Whether on the level of the individual in a simple embezzlement case, or on the scale of an entire industry in a financial crisis, the decisions finance professionals make can and do influence everyone in our global society. With this power comes great responsibility. Finance professionals should be aware of the scandals that have happened in the past, and, at a minimum, work to avoid repeating them in the future.

Citations

A Framework for Ethical Decision Making. Markkula Center for Applied Ethics. 2021.

Shefrin, Hersh. Behavioral Risk Management. Palgrave Macmillan. 2016.

Skeet, Ann. Interview with Aaron Beam: The Slippery Slope to Corporate Corruption. Markkula Center for Applied Ethics. 2018.